One thing that stands out here in Tanzania (yupp, I’m still here, greetings from Zanzibar!) is the huge wealth gap. Tourists can easily pay European prices at restaurants and hotels. Wealthy locals drive big SUVs and own generous houses (and other real estate). But many Tanzanians live in tremendously poor conditions, especially in rural areas. You’ll see improvised fishermen’s huts along the coast and farmers’ tiny mud dwellings in the interior. Many of them mostly employ subsistence agriculture. They may have less than 1 EUR per day at their disposal.

As one tourist guide book put it: you’ll probably have more cash in your pocket right now than your Tanzanian street vendor makes in a year. When dealing with chapati vendors, boda boda drivers, or even small shops and restaurants, you’ll have trouble getting correct change, because they simply do not have enough money around. And that is despite the fact that the biggest bill (10000 TZS) is currently worth less than 4 EUR. At the other end of the spectrum this means that successful local businesswomen will wander around with big piles of money, otherwise only seen in rap videos. Here’s one of my own bundles:

(Un)availability of modern technology reflects the poverty. Many people have no access to the power grid, let alone landline phones. Mobile phones on the other hand seem attractive and cheap enough that they proliferated widely. Even in remote villages, at least a few persons may have a mobile phone. In more urban areas you’ll see Android phones, presumably many of them are second-hand. You’ll still see many 90ies Nokia-style phones with little to no mobile Internet capabilities.

However, even those simple phones give access to some form of mobile banking (while most poor people cannot afford real bank accounts, credit cards, etc.). When I bought my Vodacom pre-paid SIM card, I automatically gained access to their M-Pesa service. That is a mobile phone based money-transfer and micro-payment service. While M-Pesa was one of the front-runners (originally in Kenya) all other Tanzanian mobile network operators offer similar services today.

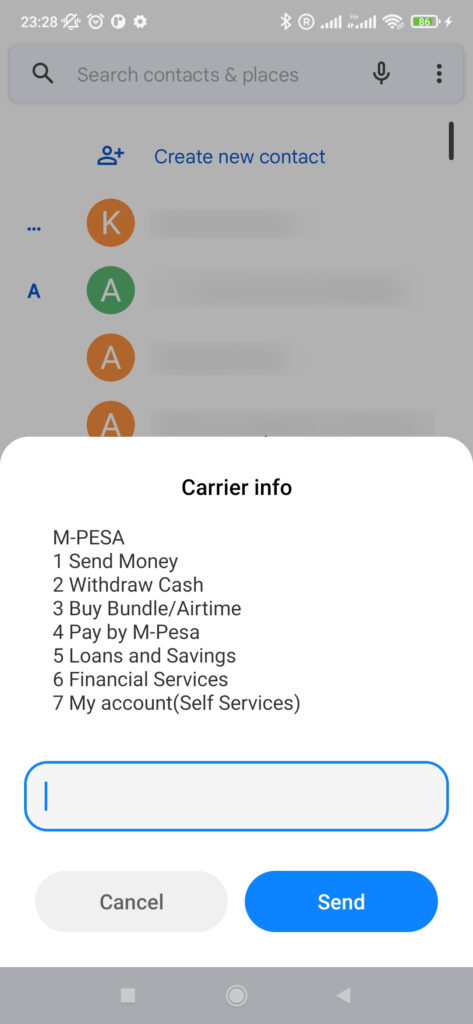

The M-Pesa service is primarily bound to your mobile phone number. While mobile apps are available, you do not need one to use M-Pesa. Instead M-Pesa can be used via USSD, an obscure (to me) part of the GSM standard. USSD is an interactive protocol: mobile phones can initiate USSD via dialing special numbers (containing lots of # and *, similar to GSM codes). Then you’ll be presented a list of options and you can select them by pressing numbers on the phone. You can also specify other numeric inputs, e.g. the amount of money or the recipient’s phone number in an M-Pesa transaction. This is what it looks like in the phone app of a modern Android phone:

Keep in mind that Android (or iOS) is not required for any of that. Most simple GSM phones will support USSD, and later 3G/4G/5G phones are backwards compatible with GSM. (Though very old GSM phones from the 90ies may not support USSD yet.) You do not need proper mobile Internet either, and if your mobile data package is billed by the byte, USSD will not count against that. However, some M-Pesa operations are subject to fees, including moderate transaction fees for sending money.

You can also transfer money between classic bank accounts or credit cards and M-Pesa. Allegedly that does not work well with foreign accounts or cards though. The main interface to the world of cash money are the abundant “Wakala” kiosks. The term Wakala seems to come from Islamic finance, but here in Tanzania, Wakala typically means this:

So far, I haven’t used M-Pesa much. Just for topping up my prepaid phone services. And for paying the entrance fee for the National Museum of Tanzania, who did not accept cash — presumably because of the Covid19 pandemic?

For the future, here is my Tanzania USSD cheat sheet:

- *150*00# — M-Pesa

- *149*01# — Vodacom prepaid services

- *#100# — Show own phone number (standard GSM code)

As an information security expert, I have to wonder how secure a payment system ultimately based on GSM can be? I’ve heard about so many problems with the underlying networking standards. But I guess that real-life attacks would require an IMSEI-catcher. Widespread fraud might just not pay off here. In particular, because M-Pesa seems to impose some limits on account balance and transaction amounts.